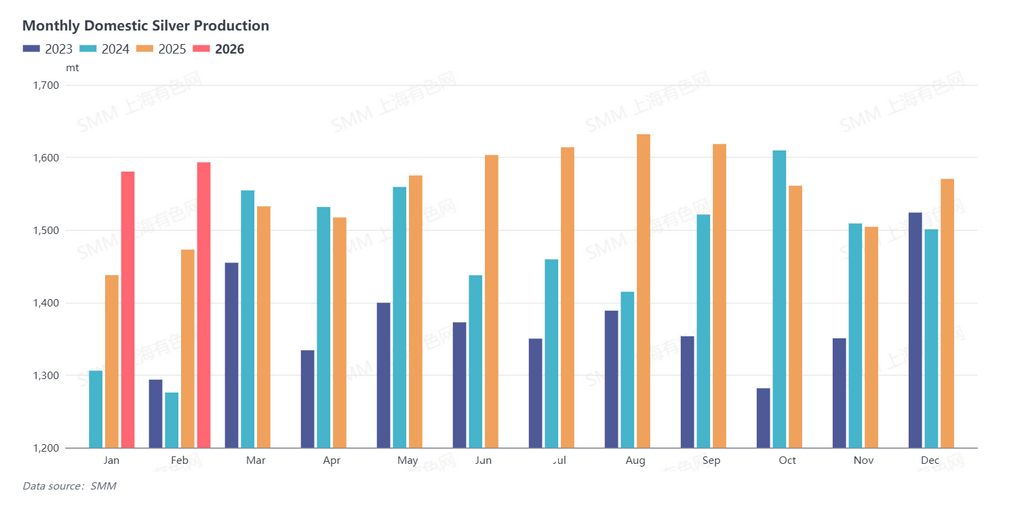

On the production side, China's 1# silver output in February 2025 increased 0.81% MoM and 8.17% YoY.

Drivers for the output increase included: most refined silver smelters maintained normal production during the Chinese New Year holiday, supported by strong market conditions such as undersupply of silver ingots and a significant rise in premiums, which boosted production enthusiasm. Some smelters noted that high-premium spot orders could cover the remelting costs of non-compliant inventory products, leading to a slight output increase. In addition, imported crude silver raw materials and large ingots arrived in bulk in February, and several smelters raised output due to increased toll processing of crude silver. A lead smelter in Jiangxi that underwent maintenance in January resumed production in February, also contributing to the increase.

Factors constraining output included: some smelters maintained their regular production pace without actively raising output for volume targets; due to fewer calendar days in February, output decreased slightly. Routine maintenance during the Chinese New Year holiday at some lead smelters in Hunan and Yunnan led to reduced supply of silver refining raw materials, and silver output in both February and March is expected to be below normal levels.

Outlook for March output: Silver ingot supply is expected to maintain positive growth. Medium- to large-scale smelters in Henan, Hunan, and Shandong have slightly raised production plans. Lead smelters that reduced output due to maintenance in February will gradually resume operations in March, with precious metal output expected to return to normal levels by late March. China's 1# silver output in March 2026 is projected to increase about 8% MoM.

On the inventory side, downstream processing enterprises generally halted operations during the Chinese New Year holiday, while refined silver smelters maintained normal operations, leading to seasonal inventory buildup of domestic silver ingots. According to an SMM survey, smelter inventory was almost transferred within one day after the holiday—either stored as social inventory or quickly shipped out via long-term contracts and spot orders for destocking. As downstream enterprises had not fully resumed work and production in the first week after the holiday, some smelters reserved several metric tons of downstream long-term contract orders pending pickup. Compared with the same period in previous years, downstream industrial and investment demand after the 2026 Chinese New Year was relatively strong. Although smelters operated normally during the holiday, the extent of inventory buildup was lower than in previous years. Domestic social inventory also showed an initial increase followed by a decline, with only a slight buildup.

![Geopolitical Risks Provided Strong Support, Platinum Rose Over 19% This Week [SMM Weekly Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)